Introduction

The AI-Driven Transformation of Banking

The banking industry is undergoing a fundamental transformation driven by Artificial Intelligence. What was once a sector characterized by physical branches, paper-based processes, and reactive security measures has evolved into a digital-first ecosystem where intelligence is embedded into every customer interaction and transaction.

In 2026, AI is not merely an add-on technology for banks—it is the operating system of modern banking. From detecting fraudulent transactions in milliseconds to providing personalized financial advice through conversational AI agents, banks are leveraging AI to enhance security, efficiency, and customer experience simultaneously.

The numbers tell a compelling story. Global banks are projected to spend over $25 billion on AI technologies in 2026, representing a compound annual growth rate of 23% since 2020. According to industry research, 85% of banks now consider AI critical to their competitive strategy, up from just 40% five years ago. In fraud detection alone, AI-powered systems are preventing an estimated $40 billion in annual losses globally, while personalized banking agents are handling over 15 billion customer interactions annually.

Leading technology organizations—including Google, Microsoft, OpenAI, and specialized fintech AI firms—are enabling banks to deploy sophisticated AI systems. Google’s Vertex AI provides machine learning infrastructure for fraud detection models, Microsoft’s Azure AI offers compliance-ready banking solutions, and OpenAI’s models are increasingly deployed for conversational banking agents that deliver personalized financial guidance at scale.

This comprehensive guide by MHTECHIN explores two critical applications of AI in modern banking:

- Fraud detection — how AI systems identify and prevent financial crime in real-time

- Personalized banking agents — how AI-powered virtual assistants transform customer engagement

We examine the latest developments of 2026, analyze benefits and challenges, and provide actionable insights for financial institutions seeking to harness AI’s transformative potential while managing risks and maintaining customer trust.

Understanding AI in Modern Banking

What is AI in Banking?

AI in banking encompasses the application of machine learning (ML), deep learning, natural language processing (NLP), computer vision, generative AI, and reinforcement learning to banking contexts. These technologies enable financial institutions to:

- Analyze vast volumes of transaction data, customer interactions, and market information in real-time

- Detect anomalies, fraud patterns, and emerging threats that would evade traditional rule-based systems

- Automate customer service, account management, and routine banking operations

- Improve customer engagement through personalization, predictive insights, and conversational interfaces

Why AI is Critical for Modern Banking

Banks today face a convergence of challenges that make AI adoption not merely advantageous but essential:

| Challenge | Description | AI Solution |

|---|---|---|

| Rising fraud and cyber threats | Financial fraud costs the global economy over $5 trillion annually, with schemes growing increasingly sophisticated | AI detects complex fraud patterns in real-time, adapting to new threats faster than rule-based systems |

| High transaction volumes | Large banks process millions of transactions daily—far beyond human monitoring capacity | AI systems analyze 100% of transactions continuously, not just samples |

| Demand for personalized services | Customers expect banking experiences tailored to their unique financial situations | AI delivers hyper-personalized recommendations and insights at scale |

| Regulatory requirements | Banks face complex, evolving compliance obligations with severe penalties for violations | AI automates monitoring, reporting, and compliance workflows |

| Margin pressure | Low interest rates and competition from fintechs compress traditional revenue streams | AI reduces operational costs while improving customer acquisition and retention |

AI in Fraud Detection

Understanding Banking Fraud

Banking fraud has become increasingly sophisticated, encompassing a wide range of criminal activities:

| Type of Fraud | Description | Example |

|---|---|---|

| Unauthorized transactions | Fraudulent transfers from legitimate accounts | Stolen credit card credentials used for online purchases |

| Identity theft | Fraudsters impersonating legitimate customers | Account takeover using stolen personal information |

| Phishing attacks | Deceptive communications tricking customers into revealing credentials | Fake bank emails directing to fraudulent websites |

| Money laundering | Concealing origins of illegally obtained money | Structuring deposits to avoid reporting thresholds |

| Application fraud | Using stolen or synthetic identities to open accounts | Fraudulent loan applications with fabricated information |

| Account takeover | Gaining unauthorized access to existing accounts | Credential stuffing attacks using stolen passwords |

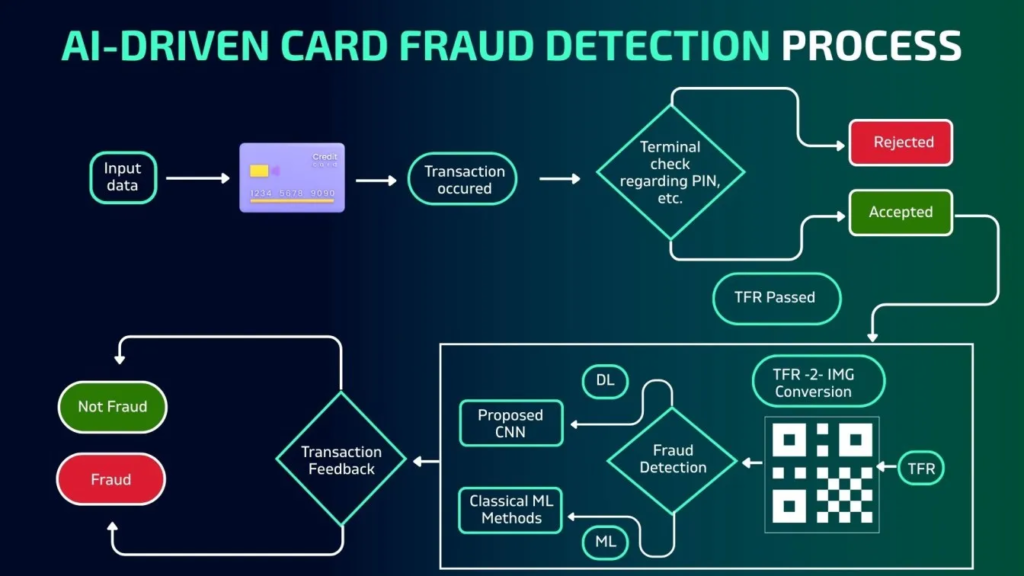

Traditional fraud detection relied on rule-based systems that flagged transactions based on predefined criteria—for example, any transaction over $5,000 or any international transfer. While these systems caught some fraud, they suffered from significant limitations:

- High false positive rates: Legitimate transactions were frequently flagged, creating customer friction and operational burden

- Inability to detect novel patterns: Rule-based systems only caught fraud that matched known patterns

- Reactive rather than predictive: Systems flagged fraud after it occurred rather than preventing it

- Manual review bottlenecks: Alert volumes overwhelmed investigators

AI-based fraud detection addresses these limitations through advanced analytics that learn, adapt, and predict.

How AI Detects Banking Fraud

Anomaly Detection

AI systems learn what constitutes “normal” behavior for each customer and transaction type, then flag deviations that may indicate fraud:

Transaction-Level Anomalies: AI models analyze individual transactions for suspicious characteristics:

- Sudden large transfers inconsistent with customer history

- Transactions from unusual geographic locations

- Transactions at atypical times (e.g., 3 AM for a customer who normally banks during business hours)

- Transactions to unfamiliar beneficiaries

- Unusual combinations (e.g., cash withdrawal followed by international transfer)

Velocity Detection: AI identifies patterns where multiple transactions occur in unusually rapid succession, potentially indicating coordinated fraud.

Device and Channel Analysis: AI tracks the devices, IP addresses, and channels used for transactions, flagging when a transaction originates from an unrecognized device even if credentials are correct.

Behavioral Analysis

Unlike traditional systems that evaluate each transaction in isolation, AI-powered behavioral analysis builds comprehensive profiles of customer behavior over time:

Spending Pattern Analysis: AI learns a customer’s typical spending categories, amounts, and frequencies. A sudden shift—such as a customer who typically spends $200 monthly on groceries suddenly spending $5,000 at electronics retailers—triggers alerts.

Transaction Sequence Analysis: AI understands normal sequences of activity. For example, if a customer typically checks their balance before making a large transfer, an AI system might flag a large transfer without the preceding balance check as suspicious.

Navigation and Interaction Patterns: Advanced systems analyze how customers navigate mobile apps and websites. A fraudster who has stolen credentials may navigate differently than the legitimate customer, even if they have the correct login information.

Location Consistency: AI analyzes whether transaction locations align with a customer’s known locations (home, work, travel patterns) and whether sequential transactions could physically occur given time and distance constraints.

Real-Time Monitoring

AI systems monitor transactions instantaneously, enabling preventive rather than reactive fraud management:

In-Transaction Decisioning: AI evaluates transactions in the milliseconds between initiation and completion, making real-time decisions to approve, flag, or block.

Adaptive Authentication: When AI detects elevated risk, it can trigger step-up authentication—requiring additional verification before allowing a transaction to proceed.

Proactive Alerts: AI systems notify customers of suspicious activity instantly, often before the customer is aware of an issue.

Automated Action: For high-confidence fraud detection, AI systems can automatically block transactions, freeze accounts, or initiate recovery procedures without waiting for human review.

Pattern Recognition and Network Analysis

AI excels at detecting complex fraud schemes that span multiple accounts, institutions, or time periods:

Graph Neural Networks: AI models analyze relationships between accounts, transactions, and entities to identify fraud rings. A graph neural network might detect that seemingly unrelated accounts share IP addresses, phone numbers, or physical addresses—revealing coordinated fraudulent activity.

Historical Fraud Pattern Matching: AI models trained on historical fraud data recognize patterns that have been used in previous attacks, even when fraudsters modify specific details.

Synthetic Identity Detection: AI analyzes identity attributes—combinations of name, address, Social Security number, and other data—to detect synthetic identities that combine real and fabricated information.

Mule Account Identification: AI identifies accounts being used to move fraudulent funds, analyzing transaction patterns that suggest money laundering or fraud proceeds.

Benefits of AI in Fraud Detection

| Benefit | Description | Impact |

|---|---|---|

| Faster detection | AI identifies fraud in milliseconds, enabling prevention rather than recovery | Reduced fraud losses, improved customer protection |

| Reduced false positives | AI systems achieve 80-90% reduction in false positives compared to rule-based systems | Fewer declined legitimate transactions, reduced operational burden |

| Real-time protection | Continuous monitoring catches fraud as it occurs, not after the fact | Prevention of unauthorized transactions before funds leave accounts |

| Improved security | AI detects sophisticated fraud schemes that evade traditional systems | Protection against emerging threats, reduced exposure |

| Adaptive capabilities | AI models continuously learn from new fraud patterns | Defenses improve over time rather than degrading |

Case Study: JPMorgan Chase AI Fraud Detection

JPMorgan Chase, one of the world’s largest banks, has deployed AI-powered fraud detection across its vast transaction network. The bank’s AI systems analyze billions of transactions annually, using machine learning models that evaluate hundreds of variables per transaction in milliseconds. The results have been significant: fraud losses reduced by over 50% while false positive rates decreased by more than 60%, improving both security and customer experience.

AI-Powered Personalized Banking Agents

What Are Personalized Banking Agents?

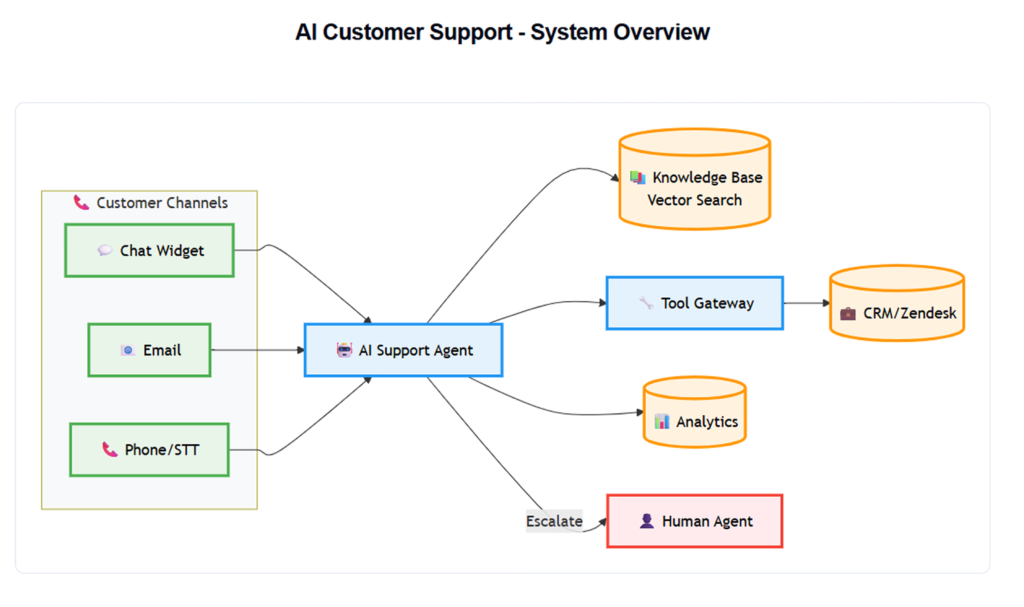

Personalized banking agents are AI-driven systems that interact with customers to provide financial advice, account management, and transaction assistance. Unlike traditional chatbots that follow scripted responses, modern AI banking agents leverage large language models (LLMs) and machine learning to deliver intelligent, context-aware, and personalized interactions.

These agents act as virtual financial assistants—available 24/7 across mobile apps, websites, voice assistants, and messaging platforms. They understand natural language, remember previous interactions, and adapt to individual customer needs over time.

Evolution of Banking Agents

| Generation | Capabilities | Limitations |

|---|---|---|

| Basic chatbots (2010-2018) | Scripted responses to common questions | Could only handle simple, predictable queries |

| Rule-based virtual assistants (2018-2022) | Decision-tree navigation, basic transaction capabilities | Limited understanding, rigid workflows |

| ML-enhanced agents (2022-2025) | Natural language understanding, personalized recommendations | Still required significant human handoff |

| Generative AI agents (2025-present) | Conversational AI, contextual memory, complex task execution | Emerging technology, integration challenges |

Today’s AI banking agents represent the fourth generation—powered by large language models that enable human-like conversation, complex reasoning, and autonomous task execution.

Key Features of AI Banking Agents

Customer Interaction Capabilities

Modern AI banking agents communicate across multiple channels with consistent, personalized experiences:

Chat-Based Assistants: Integrated into banking apps and websites, chat agents handle everything from basic inquiries to complex transactions. Customers can type questions like “What did I spend on dining last month?” or “Transfer $500 to my savings account” and receive immediate responses and actions.

Voice Assistants: AI agents support voice interactions through mobile apps, smart speakers, and phone banking systems. Natural language understanding enables customers to speak conversationally: “Hey bank, can you remind me to pay my credit card bill on the 15th?”

Omnichannel Consistency: AI agents maintain context across channels. A customer who starts a conversation on chat can switch to voice without repeating information, and the agent remembers previous interactions.

Personalized Recommendations

AI agents analyze customer data to deliver tailored financial insights and suggestions:

Savings Recommendations: By analyzing spending patterns, income, and financial goals, AI agents suggest personalized savings plans. For example: “I noticed you spend $120 monthly on unused subscriptions. Would you like help canceling these and redirecting $100 monthly to your savings goal?”

Investment Guidance: AI agents provide personalized investment recommendations aligned with customer risk tolerance, time horizon, and financial objectives. While not replacing professional advisors, they democratize access to basic investment guidance.

Budgeting Assistance: Agents categorize expenses, identify spending patterns, and suggest budget adjustments. “Your dining out spending increased 30% this month compared to your average. Would you like to set a dining budget alert?”

Product Recommendations: Based on customer behavior and needs, AI agents suggest relevant banking products—a higher-yield savings account when balances grow, a credit card with better rewards for spending patterns, or a loan product when major purchases are anticipated.

Automated Banking Services

AI agents execute transactions and manage accounts autonomously:

Balance and Transaction Inquiry: Customers ask “What’s my current balance?” or “Show me my last five transactions” and receive immediate, accurate responses.

Fund Transfers: Agents execute transfers between accounts, to external accounts, or to other customers—all through conversational commands.

Bill Payments: AI agents schedule, modify, and track bill payments. “Pay my electricity bill for $150 from checking” or “Set up automatic monthly payments for my internet bill.”

Card Management: Customers can lock lost cards, report fraud, order replacements, and manage card settings through conversational interfaces.

Account Opening: AI agents guide customers through account opening processes, collecting information, verifying identity, and completing applications without human intervention.

Financial Insights and Education

AI agents provide valuable financial intelligence:

Spending Analysis: Agents provide detailed breakdowns of spending by category, merchant, and time period. “Your highest spending categories this month were groceries ($450), dining ($320), and utilities ($210).”

Cash Flow Forecasting: AI analyzes income patterns and recurring expenses to forecast future cash positions. “Based on your current balance and upcoming bills, you’ll have approximately $1,200 remaining after all scheduled payments this month.”

Financial Health Scores: Agents calculate and explain financial health metrics, helping customers understand their overall financial position and areas for improvement.

Educational Content: When customers ask financial questions, agents provide educational explanations tailored to their knowledge level and specific situation.

Benefits of Personalized Banking Agents

| Benefit | Description |

|---|---|

| Enhanced customer experience | Natural, conversational interactions replace cumbersome menus and hold times |

| 24/7 availability | Customers receive assistance anytime, not just during business hours |

| Faster service delivery | Instant responses to queries and immediate execution of routine transactions |

| Increased customer engagement | Proactive insights and personalized recommendations keep customers engaged with their finances |

| Reduced operational costs | AI agents handle millions of routine interactions that would otherwise require human representatives |

| Scalability | AI agents scale to handle any volume of interactions without additional staffing |

Case Study: Bank of America’s Erica

Bank of America’s Erica—one of the most widely deployed AI banking agents—has served over 40 million clients since its launch. Erica handles over 1.5 million client interactions daily, performing tasks ranging from balance inquiries and bill payments to proactive alerts and financial guidance. According to Bank of America, Erica has saved customers over 200 million hours of time that would otherwise be spent navigating menus or visiting branches. The platform continues to evolve, with generative AI capabilities enabling more sophisticated conversations and proactive financial insights.

Integration of Fraud Detection and AI Agents

Creating a Secure and Interactive Banking Ecosystem

Modern banking systems integrate fraud detection capabilities with personalized AI agents, creating a unified experience that combines security with convenience:

Real-Time Fraud Alerts via AI Agents

When fraud detection systems identify suspicious activity, AI agents deliver real-time notifications through the customer’s preferred channel:

Instant Notifications: Customers receive immediate alerts about suspicious transactions via app notifications, SMS, email, or voice. The AI agent explains the nature of the suspicious activity in plain language: “We noticed a transaction for $950 at an electronics store in Miami that differs from your typical spending pattern. Did you authorize this purchase?”

Interactive Resolution: AI agents guide customers through fraud resolution processes. Instead of calling a fraud hotline and waiting on hold, customers can respond directly to the AI agent: “No, I didn’t make this purchase.” The agent then guides account blocking, card replacement, and dispute filing.

Proactive Security Guidance: AI agents provide personalized security recommendations based on detected threats. If a customer’s credentials appear in a data breach, the agent proactively recommends password changes and enhanced authentication.

AI Agents as Fraud Prevention Partners

AI banking agents serve as the frontline defense against fraud by educating and empowering customers:

Transaction Confirmation: For high-risk transactions, AI agents can initiate confirmation conversations. “I see you’re initiating a $5,000 transfer to a new beneficiary. For your security, please confirm the last four digits of the recipient’s account number.”

Security Education: When customers exhibit risky behaviors—such as using weak passwords or clicking suspicious links—AI agents provide personalized security education.

Credential Compromise Response: If AI systems detect signs of credential compromise, agents guide customers through securing their accounts, resetting passwords, and reviewing recent activity.

Integration Benefits

| Benefit | Description |

|---|---|

| Seamless customer experience | Security and service are unified—customers don’t need separate channels for fraud resolution and banking services |

| Faster fraud response | AI agents enable immediate customer engagement when suspicious activity occurs |

| Reduced customer friction | Legitimate transactions are cleared faster when customers can quickly confirm activity |

| Improved security outcomes | Customers are more likely to engage with security notifications delivered through trusted AI agents |

Challenges in AI Adoption in Banking

Data Privacy and Security

Banks manage some of the most sensitive personal and financial data. AI adoption introduces new privacy and security considerations:

Data Protection: AI systems require access to vast amounts of customer data, expanding the attack surface for potential breaches. Banks must implement robust encryption, access controls, and monitoring.

Data Minimization: Privacy regulations require that banks collect and process only data necessary for specific purposes. AI systems must be designed with data minimization principles.

Third-Party Risk: Many AI solutions rely on third-party vendors, introducing additional data security considerations. Banks must conduct rigorous vendor due diligence and maintain control over customer data.

Customer Consent: AI systems must respect customer privacy preferences and obtain appropriate consent for data usage.

Regulatory Compliance

Banks operate in one of the most heavily regulated industries. AI adoption must navigate complex regulatory requirements:

Model Risk Management: Banking regulators require rigorous model governance, including validation, documentation, and ongoing monitoring of AI models.

Explainability Requirements: AI-driven decisions—particularly those affecting credit, fraud determinations, and account actions—must be explainable to both customers and regulators.

Fair Lending Compliance: AI systems used in credit decisions must not discriminate on prohibited bases, requiring rigorous bias testing and ongoing monitoring.

Evolving Regulatory Landscape: The regulatory framework for AI continues to evolve, with new requirements emerging from bodies like the EU (AI Act), US banking regulators, and international standard-setters.

Model Transparency

The “black box” problem—where AI models produce accurate predictions without clear explanations—poses particular challenges in banking:

Customer Communication: When AI systems decline transactions, flag accounts, or make credit decisions, banks must provide clear explanations that customers can understand.

Regulatory Review: Banking regulators expect to understand how AI systems make decisions and will scrutinize models that lack transparency.

Audit Requirements: Banks must maintain comprehensive documentation of AI model development, validation, and performance for internal and external audits.

Integration with Legacy Systems

Most banks operate complex legacy infrastructures that predate modern AI:

Mainframe Systems: Core banking systems often run on mainframes with limited API capabilities, making integration with AI platforms challenging.

Data Silos: Customer data, transaction data, and operational data reside in disconnected systems, complicating the data aggregation required for AI.

Real-Time Requirements: Fraud detection requires millisecond response times that challenge some integration approaches.

Migration Complexity: Replacing legacy systems carries operational risk and requires significant investment.

Ethical Considerations

Bias in AI Models

AI models trained on historical data may perpetuate or amplify existing biases:

Fair Lending Risk: Credit models must not discriminate on race, gender, age, or other protected characteristics. Historical data may reflect past discrimination, requiring careful bias mitigation.

Representative Training Data: Models must be trained on diverse, representative data to perform equitably across all customer segments.

Ongoing Monitoring: Continuous testing for disparate impact across demographic groups is essential.

Customer Trust

Building and maintaining customer trust in AI systems is essential:

Transparency: Customers should know when AI is involved in decisions affecting them and understand how those decisions are made.

Human Fallback: Customers must have access to human representatives when they need them, particularly for complex or sensitive matters.

Reliability: AI systems must demonstrate consistent, accurate performance to earn customer confidence.

Privacy Assurance: Customers need assurance that their data is protected and used appropriately.

Accountability

Clear accountability frameworks are essential for AI in banking:

Responsibility Assignment: Banks must define who is accountable for AI-driven outcomes, particularly when adverse customer impacts occur.

Error Management: Processes must exist to identify, correct, and learn from AI errors.

Oversight Structures: Senior management and board oversight of AI systems is increasingly expected by regulators.

Future of AI in Banking

2026-2030 Trajectory

Fully Autonomous Banking Agents

Within the next five years, AI banking agents will evolve from assistants to autonomous financial managers:

Proactive Financial Management: AI agents will not just respond to requests but will proactively manage finances—optimizing cash balances, identifying savings opportunities, and executing transactions without prompting.

Goal-Based Financial Planning: Customers will set financial goals (e.g., “save for a down payment,” “retire at 60”) and AI agents will develop and execute comprehensive plans to achieve them.

Cross-Institutional Coordination: AI agents will coordinate activities across multiple financial institutions, providing a unified view and management of a customer’s complete financial picture.

Advanced Fraud Prevention

Fraud detection will become increasingly predictive and preventive:

Predictive Fraud Prevention: AI will identify fraud precursors—such as credential exposure or device compromise—and take preventive action before fraud occurs.

Biometric Behavioral Authentication: Continuous authentication based on behavioral biometrics (typing patterns, mouse movements, device interaction) will replace or supplement passwords.

Deepfake Defense: As synthetic media becomes more sophisticated, AI systems will detect deepfake attempts to impersonate customers for account takeover.

Quantum-Resistant Security: As quantum computing evolves, AI systems will implement quantum-resistant encryption and detection methods.

Hyper-Personalization

Banking experiences will become increasingly personalized:

Context-Aware Banking: AI agents will understand customer context—location, calendar, life events—to deliver timely, relevant financial insights and recommendations.

Emotional Intelligence: AI systems will recognize customer sentiment and adapt communication style accordingly, providing empathy when customers are stressed or concerned.

Life Event Management: AI agents will anticipate and prepare for major life events—college planning, home purchase, retirement—with comprehensive financial preparation.

Voice and Wearable Integration

AI banking will extend beyond phones and computers:

Voice-First Banking: Advanced voice AI will enable sophisticated banking through smart speakers, automotive systems, and wearables.

Wearable Payments: Integration with smartwatches and other wearables will enable seamless transactions with AI-powered security.

Augmented Reality Banking: AR interfaces will enable immersive financial visualization—seeing spending patterns overlaid on physical environments or virtually placing furniture in homes while managing budgets.

MHTECHIN Perspective

A Strategic Approach to AI in Banking

At MHTECHIN, we advocate a strategic, balanced approach to AI adoption in banking that combines innovation with risk management and customer focus.

Combine AI with Human Oversight

AI augments—it does not replace—human expertise and judgment:

Human-in-the-Loop Design: Critical decisions—particularly those affecting account access, large transactions, and fraud determinations—maintain human oversight.

Hybrid Service Models: AI handles routine interactions, while human representatives manage complex, sensitive, or emotionally charged situations.

AI Literacy Investment: Banks invest in training employees to work effectively alongside AI systems.

Ensure Compliance and Security

Compliance and security must be foundational:

Security by Design: Security controls integrated throughout AI development, not added after deployment.

Regulatory Engagement: Proactive engagement with regulators on AI applications, seeking guidance and sharing best practices.

Comprehensive Governance: Formal AI governance structures with clear roles, responsibilities, and accountability.

Third-Party Risk Management: Rigorous oversight of AI vendors and partners.

Focus on Personalization and User Experience

Customer experience drives adoption and value:

User-Centered Design: AI interfaces designed for customer needs, not technical capabilities.

Transparency by Default: Clear communication about AI’s role, capabilities, and limitations.

Continuous Improvement: Regular customer feedback loops to refine AI experiences.

Accessibility: AI systems designed for all customers, including those with disabilities and varying technical comfort.

Build Scalable and Secure Architectures

Technology foundations enable sustainable AI adoption:

Cloud-Native Infrastructure: Modern, scalable platforms that support AI deployment at enterprise scale.

API-First Design: Systems designed for integration with AI services and future capabilities.

Data Modernization: Investment in data infrastructure to enable AI while maintaining governance.

Operational Excellence: Robust monitoring, incident response, and continuous improvement processes.

This approach ensures sustainable AI adoption that delivers measurable value while maintaining customer trust and regulatory compliance.

Conclusion

The Intelligent Future of Banking

AI is transforming banking across every dimension—making fraud detection faster, more accurate, and more preventive while enabling personalized customer experiences that were impossible at scale just a few years ago.

In fraud detection, AI systems analyze billions of transactions in real-time, detecting complex fraud patterns that would evade traditional rule-based systems. They achieve dramatic reductions in false positives while improving detection rates, protecting both banks and customers from financial crime.

In personalized banking, AI agents serve as virtual financial assistants—available 24/7 across channels, understanding natural language, remembering context, and delivering tailored insights and recommendations. They handle millions of daily interactions, freeing human representatives for complex cases while providing customers with instant, intelligent service.

The integration of these capabilities—fraud detection and AI agents—creates a secure yet seamless banking experience. Customers receive real-time alerts about suspicious activity through the same conversational interfaces they use for everyday banking, enabling faster resolution and better security outcomes.

Challenges remain—data privacy, regulatory compliance, model transparency, and legacy system integration require ongoing attention. The organizations that succeed will be those that balance innovation with responsibility, AI capability with human judgment, and speed with security.

MHTECHIN believes that the future of banking lies in intelligent, secure systems that deliver personalized, efficient services while maintaining customer trust and regulatory compliance. By combining AI’s analytical power with human expertise and ethical governance, we can build banking systems that are not only more efficient but also more secure, more accessible, and more responsive to customer needs.

FAQ

How is AI used in banking?

AI is used in banking for fraud detection (real-time transaction monitoring, anomaly detection, behavioral analysis), personalized banking agents (virtual assistants for customer service, financial advice, transaction execution), risk assessment (credit scoring, loan underwriting), and operational automation (document processing, compliance monitoring). As of 2026, over 85% of banks consider AI critical to their competitive strategy.

How does AI detect fraud in banking?

AI detects banking fraud through multiple techniques: anomaly detection identifies transactions that deviate from normal patterns; behavioral analysis learns individual customer habits (spending, transaction timing, device usage) and flags deviations; real-time monitoring evaluates transactions in milliseconds to block suspicious activity before completion; graph neural networks identify fraud rings by analyzing relationships between accounts and transactions. AI-powered fraud detection achieves 80-90% reduction in false positives compared to traditional rule-based systems.

What are personalized banking agents?

Personalized banking agents are AI-powered virtual assistants that interact with customers through chatbots, voice assistants, and mobile apps to provide financial services. They understand natural language, remember previous interactions, and can execute transactions, provide account information, offer personalized financial recommendations (savings plans, budgeting advice), and deliver proactive insights. Bank of America’s Erica serves over 40 million clients, handling 1.5 million daily interactions.

What are the benefits of AI in banking?

Benefits include improved security through real-time fraud detection, enhanced customer experience with 24/7 personalized service, faster transaction processing, reduced operational costs (AI agents handle millions of routine interactions), better financial guidance through personalized recommendations, and increased customer engagement through proactive insights and alerts.

What are the risks of AI in banking?

Risks include data privacy and security vulnerabilities, regulatory compliance complexity, lack of model transparency (the “black box” problem), algorithmic bias that could produce unfair outcomes, integration challenges with legacy banking systems, and potential erosion of customer trust if AI systems make errors or lack explainability. Banks address these through robust governance, explainable AI techniques, bias testing, and maintaining human oversight.

Can AI replace bank tellers and customer service representatives?

AI augments but does not completely replace bank employees. AI handles routine transactions, basic inquiries, and common service requests—freeing human employees to focus on complex issues, relationship management, sensitive situations, and advisory services. Most banks maintain hybrid service models where AI handles the volume and humans handle the value-added interactions.

What is the future of AI in banking?

The future includes fully autonomous banking agents that proactively manage finances without prompting; predictive fraud prevention that stops fraud before it occurs; hyper-personalization with context-aware, emotionally intelligent AI; voice-first and wearable banking integration; and AI agents that coordinate across multiple financial institutions to provide unified financial management.

How does AI protect customer privacy in banking?

AI systems in banking implement privacy protections including data minimization (using only data necessary for specific functions), encryption (protecting data at rest and in transit), access controls (limiting who can access customer data), federated learning (training models without centralizing raw data), and compliance with regulations like GDPR and CCPA. Banks must also obtain appropriate customer consent and provide transparency about AI data usage.

Leave a Reply